library(ggplot2)

library(gridExtra)

# --- 1. MATRIX SETUP ---

# Symmetric Matrix where eigenvectors are tilted

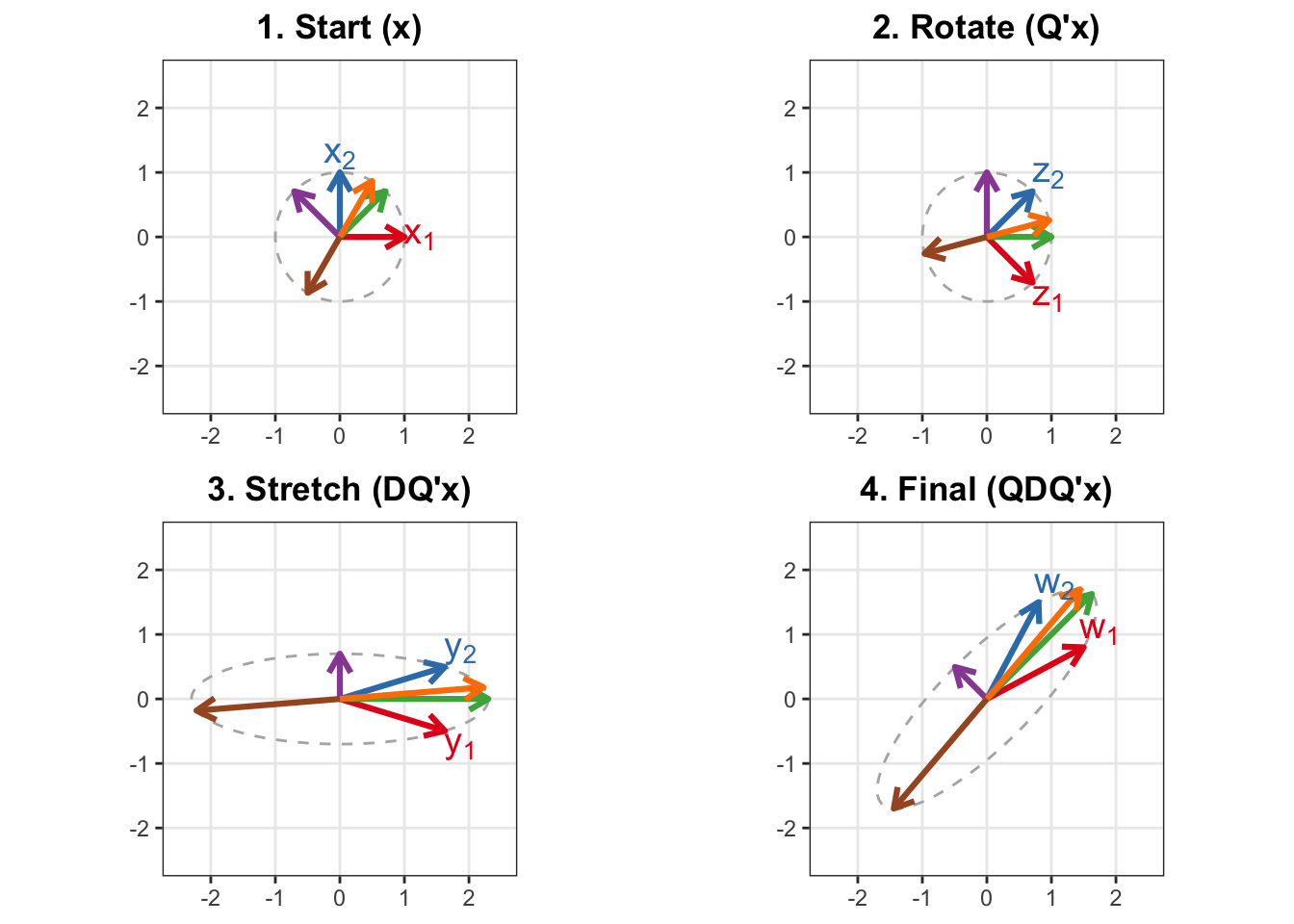

A <- matrix(c(1.5, 0.8, 0.8, 1.5), nrow = 2)

# Decomposition A = QDQ'

eig <- eigen(A)

Q <- eig$vectors

D_mat <- diag(eig$values)

# --- 2. DEFINE THE 6 VECTORS ---

# 1 & 2: Standard Axes (We will label these x1, x2)

v1 <- c(1, 0)

v2 <- c(0, 1)

# 3 & 4: Eigenvectors

v3 <- Q[,1]

v4 <- Q[,2]

# 5 & 6: Filler vectors at random angles

v5 <- c(cos(pi/3), sin(pi/3))

v6 <- c(cos(4*pi/3), sin(4*pi/3))

# Combine into starting matrix V_start

V_start <- cbind(v1, v2, v3, v4, v5, v6)

# Define 6 Distinct Colors

my_colors <- c("#E41A1C", "#377EB8", "#4DAF4A", "#984EA3", "#FF7F00", "#A65628")

names(my_colors) <- 1:6

# Background Circle Points used for reference path in all plots

theta_c <- seq(0, 2*pi, length.out = 150)

C_start <- rbind(cos(theta_c), sin(theta_c))

# --- 3. DATA PROCESSING HELPER FUNCTION ---

# This function prepares the data frames for ggplot for a given stage

prepare_data <- function(V_mat, C_mat, stage_title, label_text_pair) {

# Prepare Vectors data frame

df_v <- data.frame(t(V_mat))

colnames(df_v) <- c("x", "y")

df_v$vec_id <- factor(1:6) # Unique ID for coloring

# Add labels only for vector 1 and 2

df_v$label <- ""

df_v$label[1] <- label_text_pair[1]

df_v$label[2] <- label_text_pair[2]

# Calculate nudge for labels based on vector direction so they don't overlap arrow tip

df_v$nudge_x <- sign(df_v$x) * 0.25

df_v$nudge_y <- sign(df_v$y) * 0.25

# Don't nudge unlabelled vectors

df_v$nudge_x[3:6] <- 0

df_v$nudge_y[3:6] <- 0

# Prepare Background Path data frame

df_c <- data.frame(t(C_mat))

colnames(df_c) <- c("px", "py")

list(vecs = df_v, path = df_c, title = stage_title)

}

# --- 4. PERFORM TRANSFORMATIONS ---

# Stage 1: Start (x)

d1 <- prepare_data(V_start, C_start,

"1. Start (x)", c("x[1]", "x[2]"))

# Stage 2: Rotate (Q'x)

V2 <- t(Q) %*% V_start

C2 <- t(Q) %*% C_start

d2 <- prepare_data(V2, C2,

"2. Rotate (Q'x)", c("z[1]", "z[2]"))

# Stage 3: Stretch (DQ'x)

V3 <- D_mat %*% V2

C3 <- D_mat %*% C2

d3 <- prepare_data(V3, C3,

"3. Stretch (DQ'x)", c("y[1]", "y[2]"))

# Stage 4: Rotate Back (QDQ'x)

V4 <- Q %*% V3

C4 <- Q %*% C3

d4 <- prepare_data(V4, C4,

"4. Final (QDQ'x)", c("w[1]", "w[2]"))

# --- 5. PLOTTING FUNCTION ---

plot_stage_final <- function(data_list) {

ggplot() +

# Background path (gray dashed)

geom_path(data = data_list$path, aes(x=px, y=py),

color="gray70", linetype="dashed") +

# The 6 vectors

geom_segment(data = data_list$vecs, aes(x=0, y=0, xend=x, yend=y, color=vec_id),

arrow = arrow(length = unit(0.3, "cm")), size=1.1) +

# The labels for v1 and v2 using parsed expressions for subscripts

geom_text(data = data_list$vecs, aes(x=x, y=y, label=label, color=vec_id),

parse = TRUE, fontface="bold", size=5,

nudge_x = data_list$vecs$nudge_x,

nudge_y = data_list$vecs$nudge_y) +

scale_color_manual(values = my_colors) +

# Fixed coordinates to ensure realistic rotation/stretching view

coord_fixed(xlim = c(-2.5, 2.5), ylim = c(-2.5, 2.5)) +

theme_bw() +

theme(legend.position = "none",

panel.grid.minor = element_blank(),

plot.title = element_text(face="bold", hjust=0.5),

axis.title = element_blank()) +

labs(title = data_list$title)

}

# Generate the 4 plots

p1 <- plot_stage_final(d1)

p2 <- plot_stage_final(d2)

p3 <- plot_stage_final(d3)

p4 <- plot_stage_final(d4)

# Arrange them in a grid

grid.arrange(p1, p2, p3, p4, nrow = 2)