Code

require("knitr")

knitr::opts_chunk$set(

comment = "#",

fig.width = 6,

fig.height = 6,

cache = TRUE

)

set.seed(47)

options(sim_rebuild=FALSE)require("knitr")

knitr::opts_chunk$set(

comment = "#",

fig.width = 6,

fig.height = 6,

cache = TRUE

)

set.seed(47)

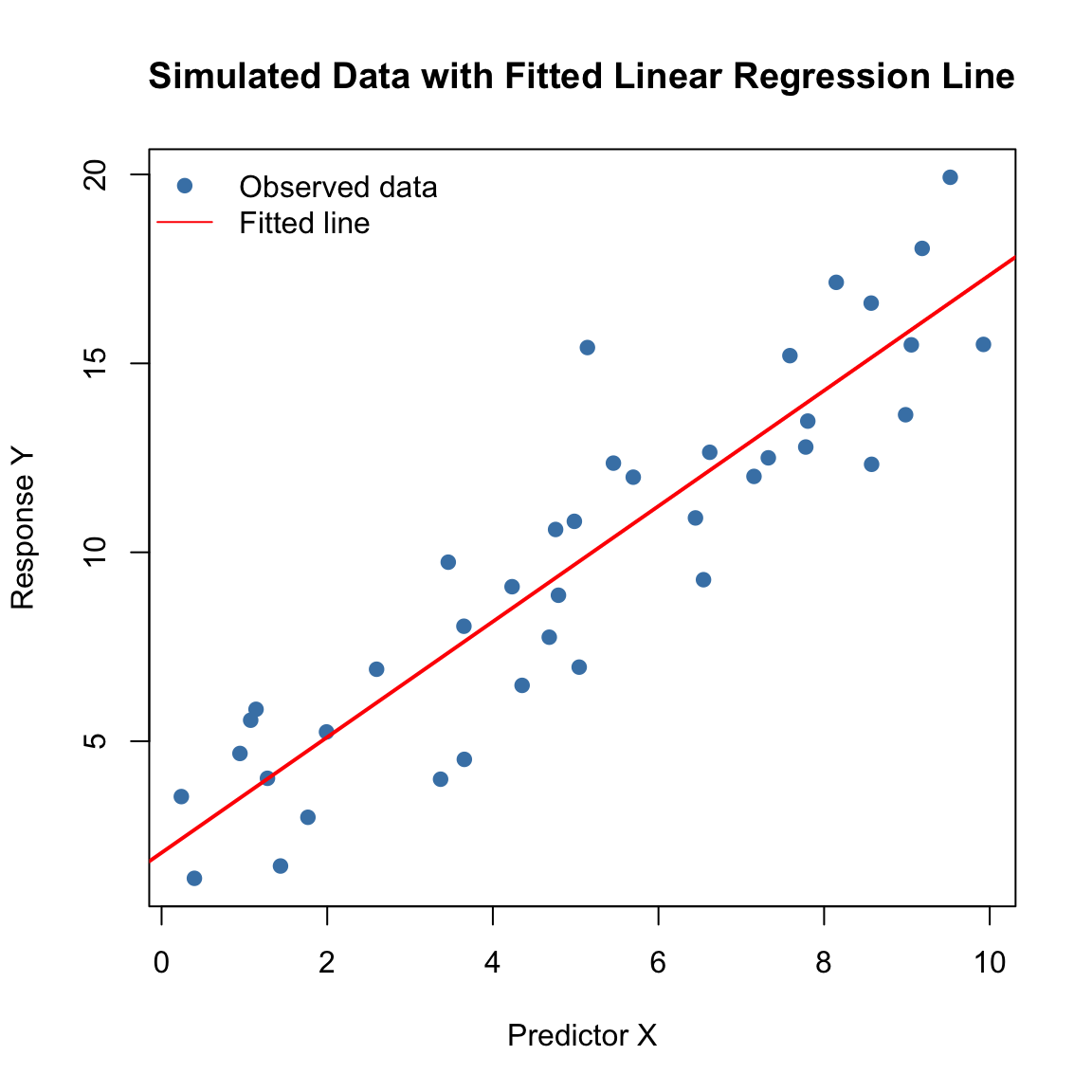

options(sim_rebuild=FALSE)To make the simple linear regression model concrete, let’s first visualize a simulated dataset that follows \[ Y_i = \beta_0 + \beta_1 X_i + \varepsilon_i, \qquad \varepsilon_i \sim \mathcal N(0, \sigma^2). \]

Here, \(\beta_0\) is the intercept, \(\beta_1\) is the slope, and \(\varepsilon_i\) represents random noise.

set.seed(2025)

n <- 40

beta0 <- 2; beta1 <- 1.5; sigma <- 2

x <- runif(n, 0, 10)

y <- beta0 + beta1 * x + rnorm(n, 0, sigma)

dat <- data.frame(x, y)

fit <- lm(y ~ x, data = dat)

plot(x, y, pch = 19, col = "steelblue",

xlab = "Predictor X", ylab = "Response Y",

main = "Simulated Data with Fitted Linear Regression Line")

abline(fit, col = "red", lwd = 2)

legend("topleft", legend = c("Observed data", "Fitted line"),

pch = c(19, NA), lty = c(NA, 1), col = c("steelblue", "red"), bty = "n")

The scatterplot shows data points scattered around a line — the red line is the fitted regression model.

Goal: Find \(\hat\beta_0\) and \(\hat\beta_1\) that minimize \[ \mathrm{SSE} = \sum_{i=1}^n (y_i - \hat\beta_0 - \hat\beta_1 x_i)^2. \]

Solutions: \[ \hat\beta_1 = \frac{\sum_i (x_i - \bar x)(y_i - \bar y)}{\sum_i (x_i - \bar x)^2} = \frac{S_{xy}}{S_{xx}}, \qquad \hat\beta_0 = \bar y - \hat\beta_1\,\bar x. \]

Here \[ S_{xy} = \sum_i (x_i - \bar x)(y_i - \bar y), \qquad S_{xx} = \sum_i (x_i - \bar x)^2. \]

Shortcut (computational) formulas: \[ S_{xy} = \sum_i x_i y_i - n\,\bar x\,\bar y, \qquad S_{xx} = \sum_i x_i^2 - n\,\bar x^2. \]

Interpretation:

- \(\hat\beta_1\) measures the estimated change in \(Y\) for each unit increase in \(X\).

- \(\hat\beta_0\) represents the fitted value of \(Y\) when \(X=0\).

Let \(\hat y_i = \hat\beta_0 + \hat\beta_1 x_i\) and \(e_i = y_i - \hat y_i\).

| Symbol | Definition | Computing Formula (in terms of \(S_{xx}, S_{xy}\), etc.) |

|---|---|---|

| SST | Total Sum of Squares | \(\displaystyle \sum_i (y_i - \bar y)^2 = S_{yy} = \sum_i y_i^2 - n\,\bar y^2\) |

| SSR | Regression Sum of Squares | \(\displaystyle \sum_i (\hat y_i - \bar y)^2 = \hat\beta_1^2 S_{xx} = \frac{S_{xy}^2}{S_{xx}}\) |

| SSE | Error (Residual) Sum of Squares | \(\displaystyle \sum_i (y_i - \hat y_i)^2 = S_{yy} - \frac{S_{xy}^2}{S_{xx}}\) |

Identity: \[ \mathrm{SST} = \mathrm{SSR} + \mathrm{SSE}. \]

Here, \[ S_{xx} = \sum_i (x_i - \bar x)^2 = \sum_i x_i^2 - n\bar x^2, \qquad S_{yy} = \sum_i (y_i - \bar y)^2 = \sum_i y_i^2 - n\bar y^2, \qquad S_{xy} = \sum_i (x_i - \bar x)(y_i - \bar y) = \sum_i x_i y_i - n\bar x \bar y. \]

Measures the proportion of total variation in \(Y\) explained by \(X\): \[ R^2 = \frac{\mathrm{SSR}}{\mathrm{SST}} = 1 - \frac{\mathrm{SSE}}{\mathrm{SST}}. \]

Interpretation:

Tests whether \(X\) is linearly related to \(Y\).

Hypotheses: \[ H_0: \beta_1 = 0 \quad \text{vs.} \quad H_A: \beta_1 \ne 0. \]

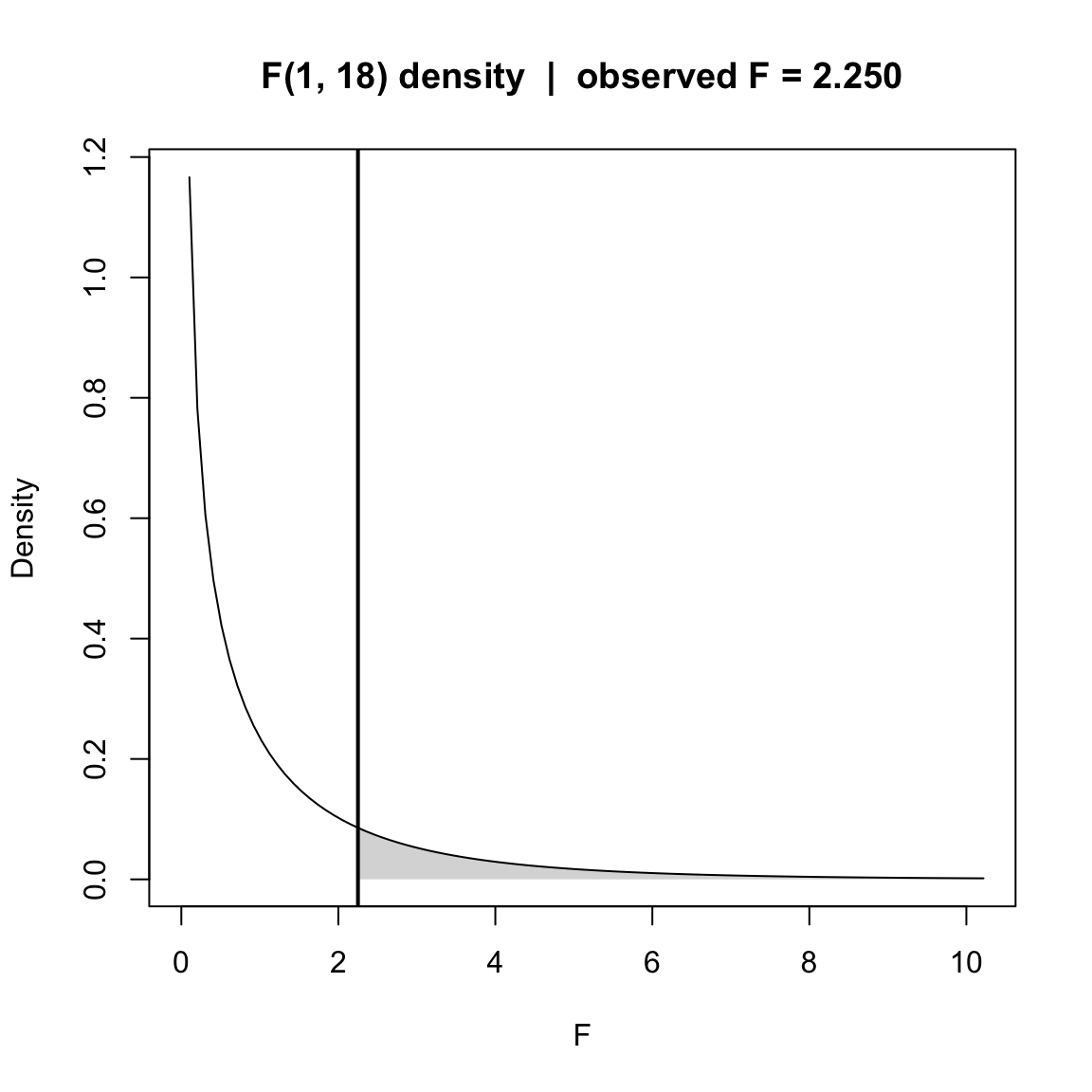

Test Statistic: \[ F = \frac{\text{MSR}}{\text{MSE}} = \frac{\text{SSR}/1}{\text{SSE}/(n-2)} \sim F_{1,n-2}\quad (H_0). \]

p-value approach for observe \(F^{\mathrm{obs}}\):

Given the observed statistic \(F^{\text{obs}}\) with \((1,\,n-2)\) df, \[ p-\text{value} \;=\; \Pr\!\big(F_{1,\,n-2} \ge F^{\text{obs}}\big) \;=\; \mathrm{pf}\!\big(F^{\text{obs}},\,1,\,n-2,\ \text{lower.tail}= \mathrm{FALSE}\big). \]

## -- Inputs (provide these from your analysis context) -------------------------

## n <- ... # sample size

## SSR <- ... # regression sum of squares

## SSE <- ... # error sum of squares

n <- 20

SSR <- 5

SSE <- 40

df1 <- 1

df2 <- n - 2

Fobs <- (SSR/df1) / (SSE/df2) # observed F

pval <- pf(Fobs, df1 = df1, df2 = df2, lower.tail = FALSE)

pval[1] 0.1509505## -- Plot F density and shade the p-value tail (with proper annotations) -------

xmax <- max(qf(0.995, df1, df2), Fobs * 1.2) # extra space for labels

peak <- max(df(seq(0, xmax, length.out = 500), df1, df2))

## Density curve

curve(df(x, df1, df2), from = 0, to = xmax,

xlab = "F", ylab = "Density",

main = sprintf("F(%d, %d) density | observed F = %.3f", df1, df2, Fobs))

## Shade right tail (p-value region)

xs <- seq(Fobs, xmax, length.out = 300)

ys <- df(xs, df1, df2)

polygon(c(Fobs, xs, xmax), c(0, ys, 0),

col = rgb(0, 0, 0, 0.18), border = NA)

## Vertical line at Fobs (optional visual aid)

abline(v = Fobs, lwd = 2)

## ---- Annotation for F^obs pointing to the x-axis value (Fobs, 0) -------------

x_txt_F <- Fobs + 0.06 * xmax

y_txt_F <- 0.45 * peak

arrows(x0 = x_txt_F, y0 = y_txt_F, x1 = Fobs, y1 = 0,

length = 0.08, lwd = 1.5)

text(x_txt_F, y_txt_F,

labels = bquote(F^{obs} == .(format(Fobs, digits = 3))),

pos = 4)

## ---- Annotation for p-value pointing into the shaded tail --------------------

x_tip_p <- (Fobs + xmax) / 1.7

y_tip_p <- df(x_tip_p, df1, df2)

x_txt_p <- Fobs + 0.08 * xmax

y_txt_p <- 0.80 * peak

arrows(x0 = x_txt_p, y0 = y_txt_p, x1 = x_tip_p, y1 = y_tip_p,

length = 0.08, lwd = 1.5)

text(x_txt_p, y_txt_p,

labels = bquote(p == .(format(pval, digits = 4, scientific = TRUE))),

pos = 4)

Equivalent to the \(F\)-test in simple regression since \(t^2 = F\).

Formula: \[ t = \frac{\hat\beta_1}{\operatorname{SE}(\hat\beta_1)}, \qquad \operatorname{SE}(\hat\beta_1) = \sqrt{\frac{\hat\sigma^2}{\sum_i (x_i - \bar x)^2}}, \qquad \hat\sigma^2 = \frac{\mathrm{SSE}}{n-2}. \]

Distribution: \[ t \sim t_{n-2}\quad (H_0:\beta_1=0). \]

Predicted mean response: \[ \hat y(x_0) = \hat\beta_0 + \hat\beta_1 x_0. \]

95% Confidence interval for mean response: \[ \hat y(x_0) \pm t_{1-\alpha/2,,n-2}, \hat\sigma,\sqrt{\frac{1}{n} + \frac{(x_0 - \bar x)^2}{\sum_i (x_i - \bar x)^2}}. \]

95% Prediction interval for a new observation: \[ \hat y(x_0) \pm t_{1-\alpha/2,,n-2}, \hat\sigma,\sqrt{1 + \frac{1}{n} + \frac{(x_0 - \bar x)^2}{\sum_i (x_i - \bar x)^2}}. \]

Summary Cheat Sheet

| Concept | Key Formula |

|---|---|

| Model | \(Y_i = \beta_0 + \beta_1 X_i + \varepsilon_i\) |

| LS Estimates | \(\hat\beta_1 = S_{xy}/S_{xx}\), \(\hat\beta_0 = \bar y - \hat\beta_1\bar x\) |

| Decomposition | \(\mathrm{SST} = \mathrm{SSR} + \mathrm{SSE}\) |

| \(R^2\) | \(R^2 = 1 - \mathrm{SSE}/\mathrm{SST}\) |

| \(F\)-test | \(F = (\mathrm{SSR}/1)/(\mathrm{SSE}/(n-2))\) |

| \(t\)-test | \(t = \hat\beta_1 / \operatorname{SE}(\hat\beta_1)\) |

| Prediction | \(\hat y(x_0) = \hat\beta_0 + \hat\beta_1 x_0\) |

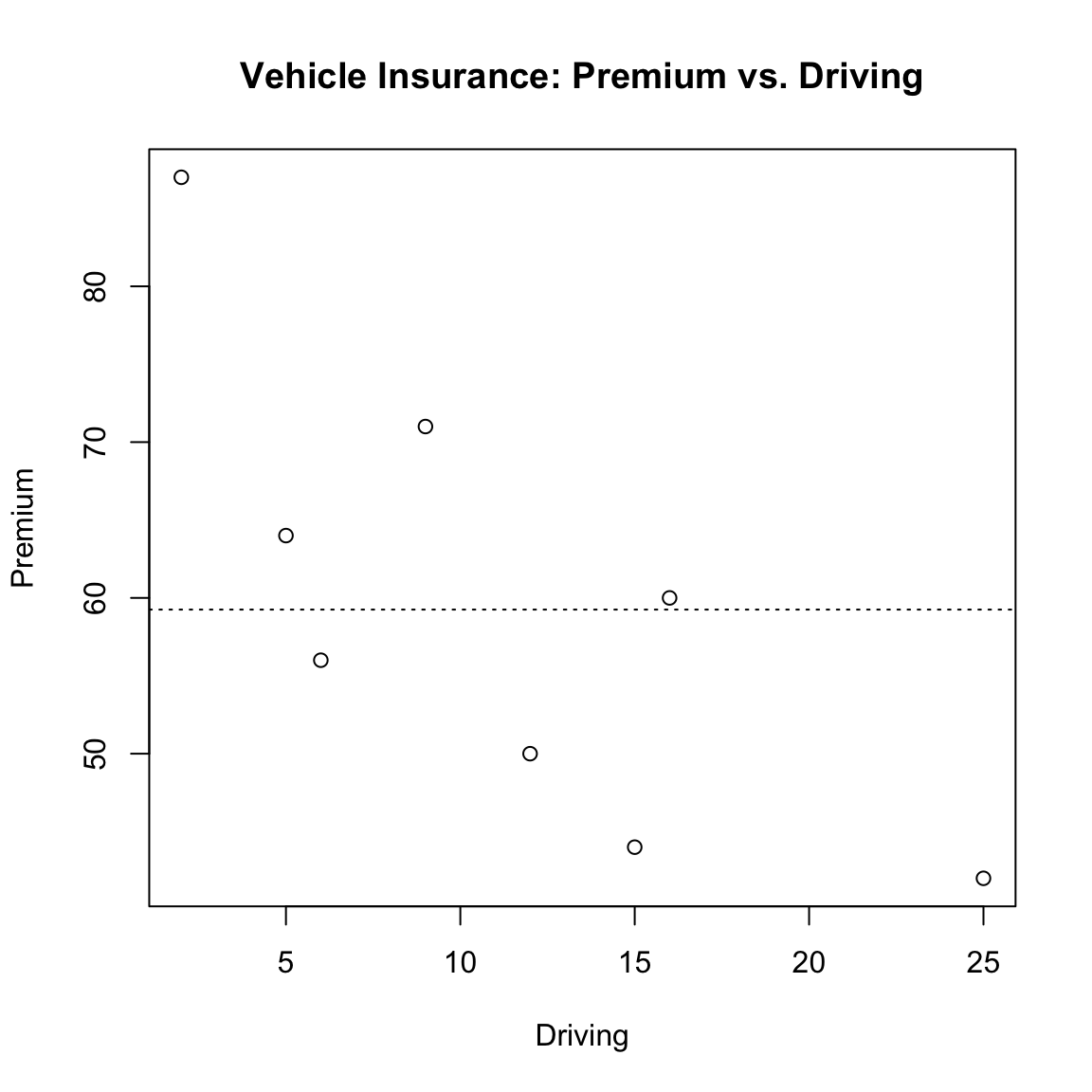

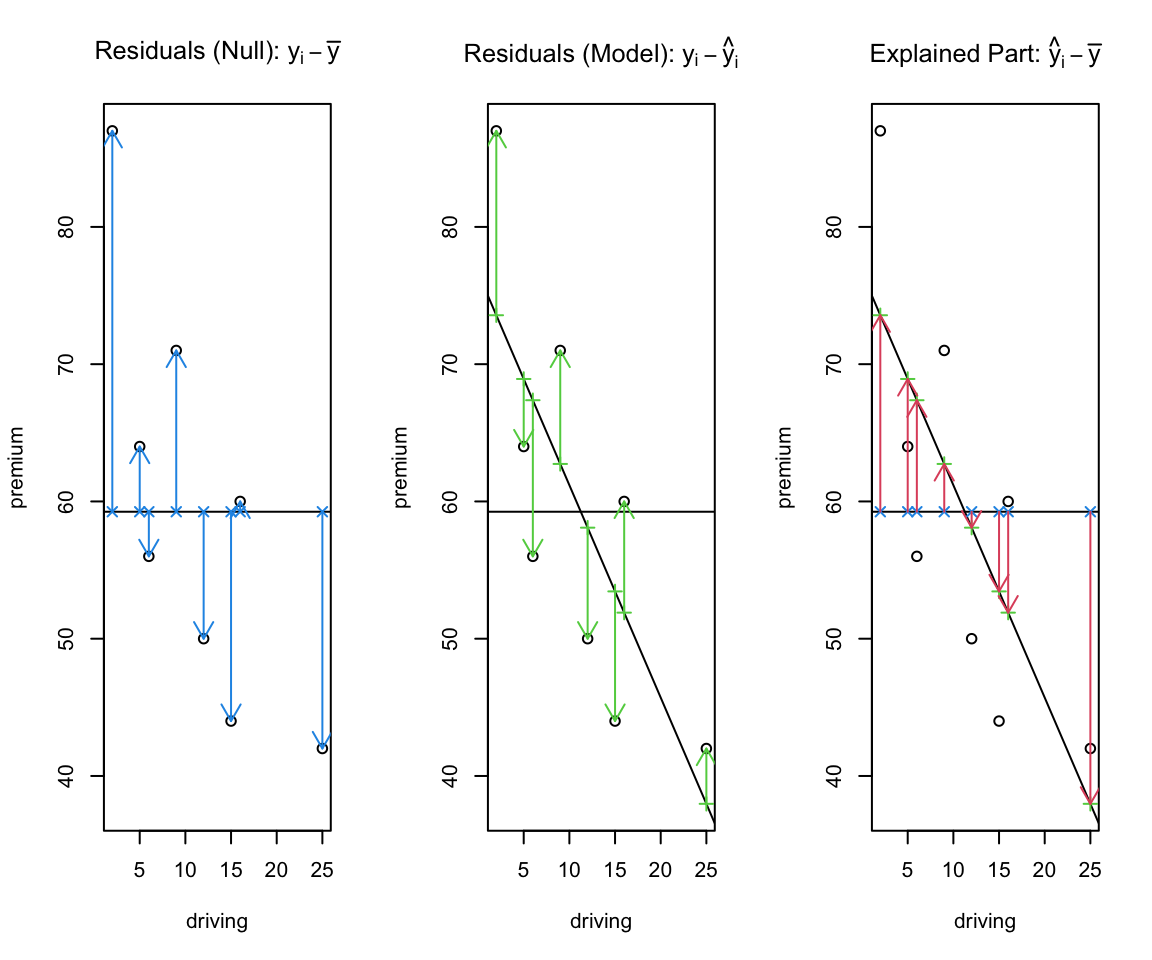

We examine premiums \(y\) vs. driving amount \(x\). The scatterplot hints at a downward trend.

issu <- data.frame(

driving = c(5, 2, 12, 9, 15, 6, 25, 16),

premium = c(64, 87, 50, 71, 44, 56, 42, 60)

)

y <- issu$premium

x <- issu$driving

xbar <- mean(x); ybar <- mean(y); n <- length(y)

plot(x, y, xlab = "Driving", ylab = "Premium",

main = "Vehicle Insurance: Premium vs. Driving")

abline(h = ybar, lty = 3)

Narrative. The horizontal line at \(\bar y\) represents the intercept-only model. Any fitted line that tilts away from this must earn its keep by reducing residual variation enough to offset the loss of one degree of freedom.

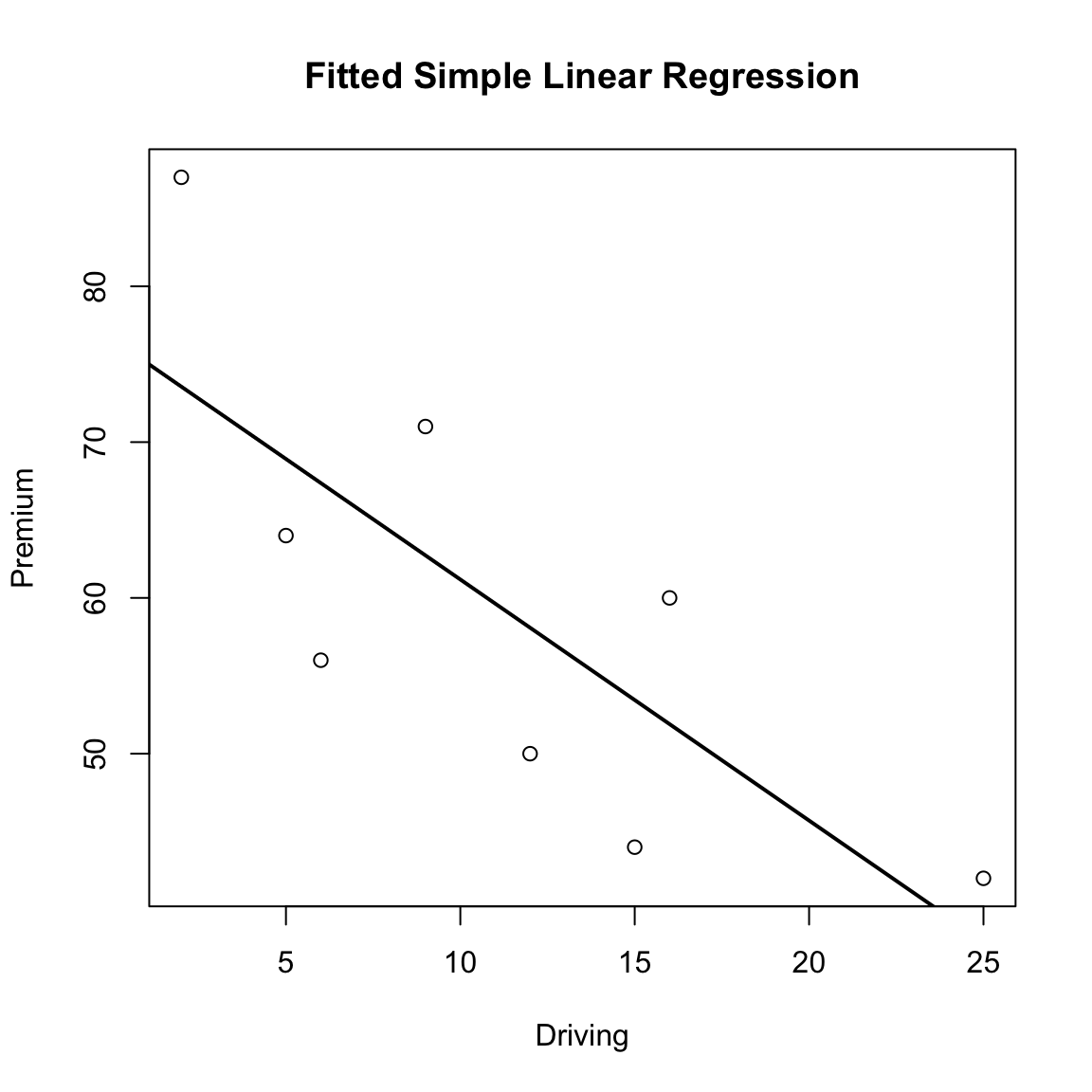

fit.issu <- lm(y ~ x)

plot(x, y, xlab = "Driving", ylab = "Premium",

main = "Fitted Simple Linear Regression")

abline(fit.issu, lwd = 2)

The slope estimate \(\hat\beta_1\) captures the marginal change in premium per unit of driving (units of \(y\) per unit of \(x\)). Inference on \(\beta_1\) tells us whether the pattern rises above noise.

Let \(\hat y_i=\hat\beta_0+\hat\beta_1 x_i\) and \(\tilde y_i=\bar y\). Residuals are \(e_i=y_i-\hat y_i\) (model) and \(y_i-\bar y\) (null). Visualizing all three clarifies the ANOVA identity.

beta0 <- coef(fit.issu)[1]

beta1 <- coef(fit.issu)[2]

fitted1 <- beta0 + beta1 * x

fitted0 <- rep(ybar, n)

residual1 <- y - fitted1

residual0 <- y - fitted0

data.frame(y, fitted0, residual0, fitted1, residual1,

diff.fitted = fitted1 - fitted0)

SST <- sum((y - fitted0)^2); SST[1] 1557.5SSE <- sum((y - fitted1)^2); SSE[1] 639.0065SSR <- SST - SSE; SSR[1] 918.4935Direct check: \(\text{SSR}=\sum(\hat y_i-\bar y)^2\).

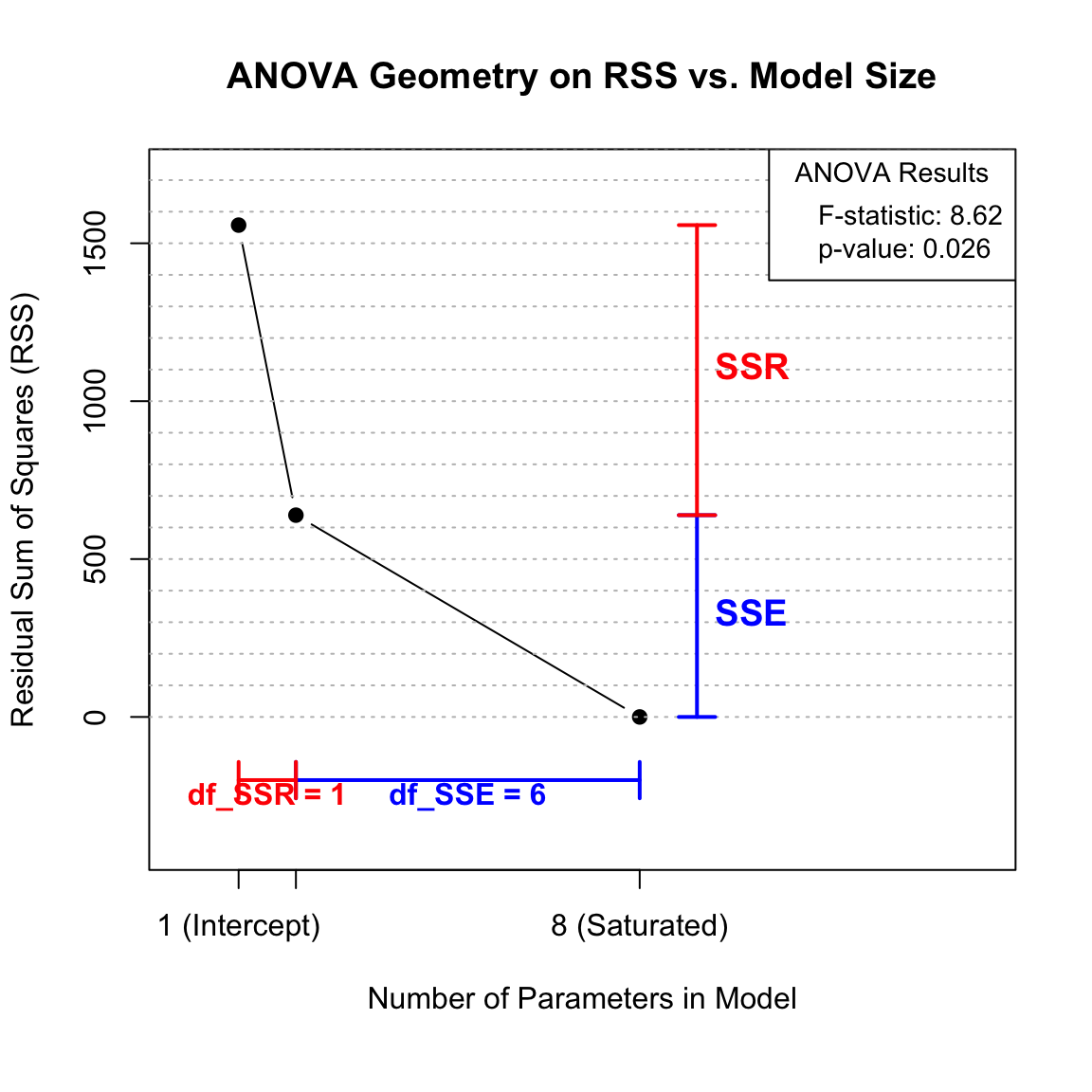

sum((fitted1 - fitted0)^2)[1] 918.4935We place the residual sum of squares against model dimension to show the trade-off between fit and df.

## Recompute cleanly

SST <- sum((y - mean(y))^2)

SSE <- sum(resid(fit.issu)^2)

SSR <- SST - SSE

df_SSR <- 1

df_SSE <- n - 2

par(mar = c(6, 4, 4, 2) + 0.1)

plot(c(1, 2, n), c(SST, SSE, 0), type = "b", pch = 19,

xlab = "Number of Parameters in Model",

ylab = "Residual Sum of Squares (RSS)",

main = "ANOVA Geometry on RSS vs. Model Size",

xlim = c(0, 14), ylim = c(-400, SST * 1.1), xaxt = "n")

axis(1, at = c(1, 2, n), labels = c("1 (Intercept)", "2 (+Slope)", paste(n, "(Saturated)")))

abline(h = seq(0, 2000, by = 100), lty = 3, col = "grey")

par(xpd = TRUE)

arrows(9, 0, 9, SSE, col = "blue", code = 3, angle = 90, length = 0.1, lwd = 2)

text(9, SSE/2, "SSE", col = "blue", pos = 4, font = 2, cex = 1.2)

arrows(9, SSE, 9, SST, col = "red", code = 3, angle = 90, length = 0.1, lwd = 2)

text(9, (SST + SSE)/2, "SSR", col = "red", pos = 4, font = 2, cex = 1.2)

arrows(2, -200, n, -200, col = "blue", code = 3, angle = 90, length = 0.1, lwd = 2)

text((2 + n)/2, -250, paste("df_SSE =", df_SSE), col = "blue", font = 2)

arrows(1, -200, 2, -200, col = "red", code = 3, angle = 90, length = 0.1, lwd = 2)

text(1.5, -250, paste("df_SSR =", df_SSR), col = "red", font = 2)

par(xpd = FALSE)

f_value <- (SSR/df_SSR) / (SSE/df_SSE)

p_value <- pf(f_value, df1 = df_SSR, df2 = df_SSE, lower.tail = FALSE)

legend("topright",

legend = c(sprintf("F-statistic: %.2f", f_value),

sprintf("p-value: %.3f", p_value)),

title = "ANOVA Results", bty = "o", cex = 0.9)

R2 <- SSR / SST; R2[1] 0.5897229f <- (SSR/1) / (SSE/(n-2)); f[1] 8.624264pvf <- pf(f, df1 = 1, df2 = n-2, lower.tail = FALSE); pvf[1] 0.0260588Ftable <- data.frame(

Source = c("Regression", "Error"),

df = c(1, n - 2),

SS = c(SSR, SSE),

MS = c(SSR/1, SSE/(n-2)),

F = c(f, NA),

pvalue = c(pvf, NA),

R2part = c(SSR, SSE) / SST

)

FtableA call to anova() reproduces the same test:

anova(fit.issu)Under \(H_0:\beta_1=0\), \(F\) follows \(F_{1,n-2}\). Under \(H_A\), the distribution shifts right (noncentral \(F\)).

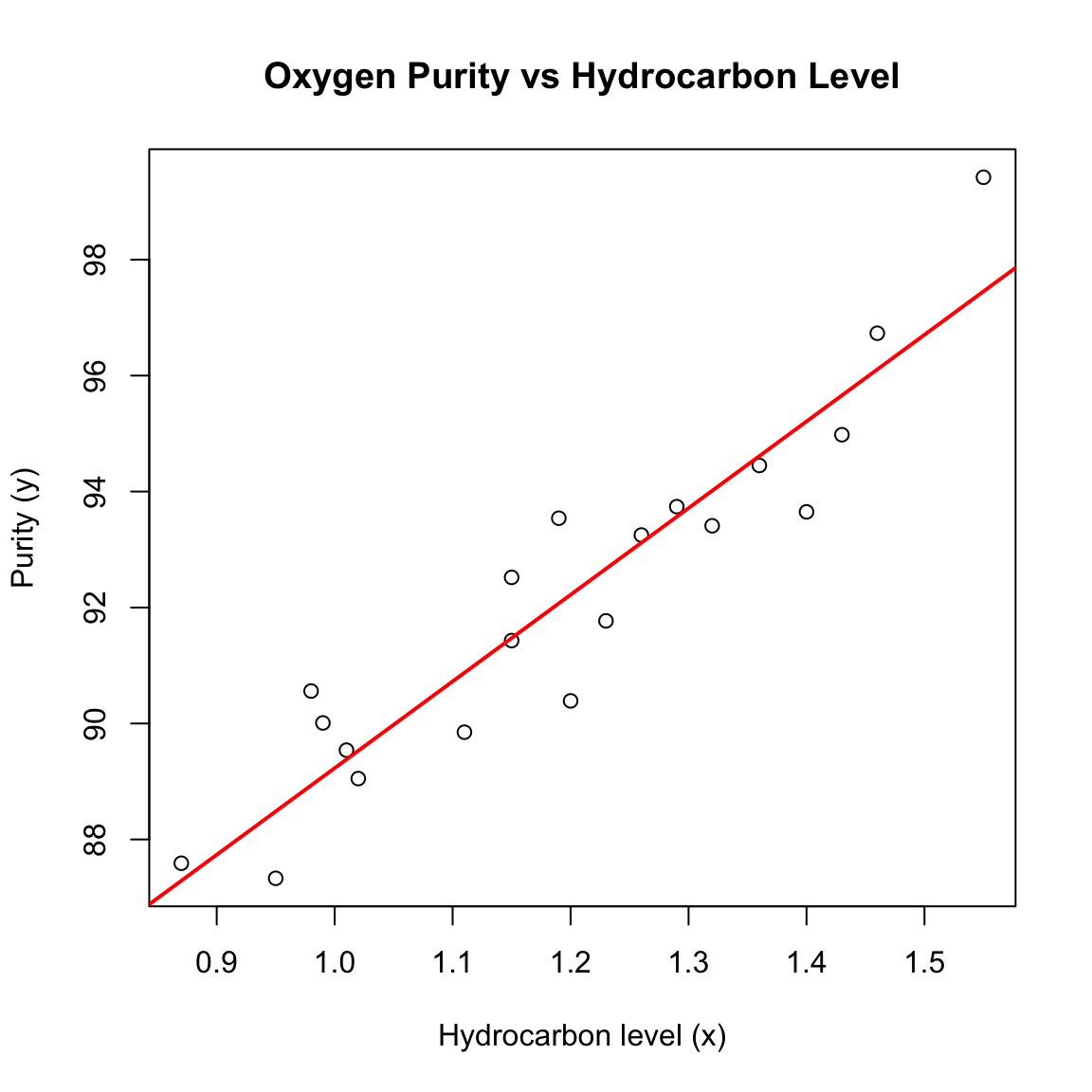

We model oxygen purity \(y\) as a function of hydrocarbon level \(x\) and report both mean response and prediction uncertainty.

x <- c(0.99, 1.02, 1.15, 1.29, 1.46, 1.36, 0.87, 1.23, 1.55, 1.40, 1.19,

1.15, 0.98, 1.01, 1.11, 1.20, 1.26, 1.32, 1.43, 0.95)

y <- c(90.01, 89.05, 91.43, 93.74, 96.73, 94.45, 87.59, 91.77, 99.42, 93.65,

93.54, 92.52, 90.56, 89.54, 89.85, 90.39, 93.25, 93.41, 94.98, 87.33)

n <- length(x); n[1] 20purity.data <- data.frame(x = x, y = y)

head(purity.data)fit <- lm(y ~ x, data = purity.data)

summary(fit)

Call:

lm(formula = y ~ x, data = purity.data)

Residuals:

Min 1Q Median 3Q Max

-1.83029 -0.73334 0.04497 0.69969 1.96809

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 74.283 1.593 46.62 < 2e-16 ***

x 14.947 1.317 11.35 1.23e-09 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.087 on 18 degrees of freedom

Multiple R-squared: 0.8774, Adjusted R-squared: 0.8706

F-statistic: 128.9 on 1 and 18 DF, p-value: 1.227e-09Interpretation. The slope’s sign gives the direction of association; its \(t\) test (or \(F\) with 1 df) assesses evidence for a trend. Look at \(\hat\sigma\) for noise scale and \(R^2\) for variance explained.

plot(purity.data$x, purity.data$y,

xlab = "Hydrocarbon level (x)", ylab = "Purity (y)",

main = "Oxygen Purity vs Hydrocarbon Level")

abline(fit, col = "red", lwd = 2)

confint(fit, level = 0.95) 2.5 % 97.5 %

(Intercept) 70.93555 77.63108

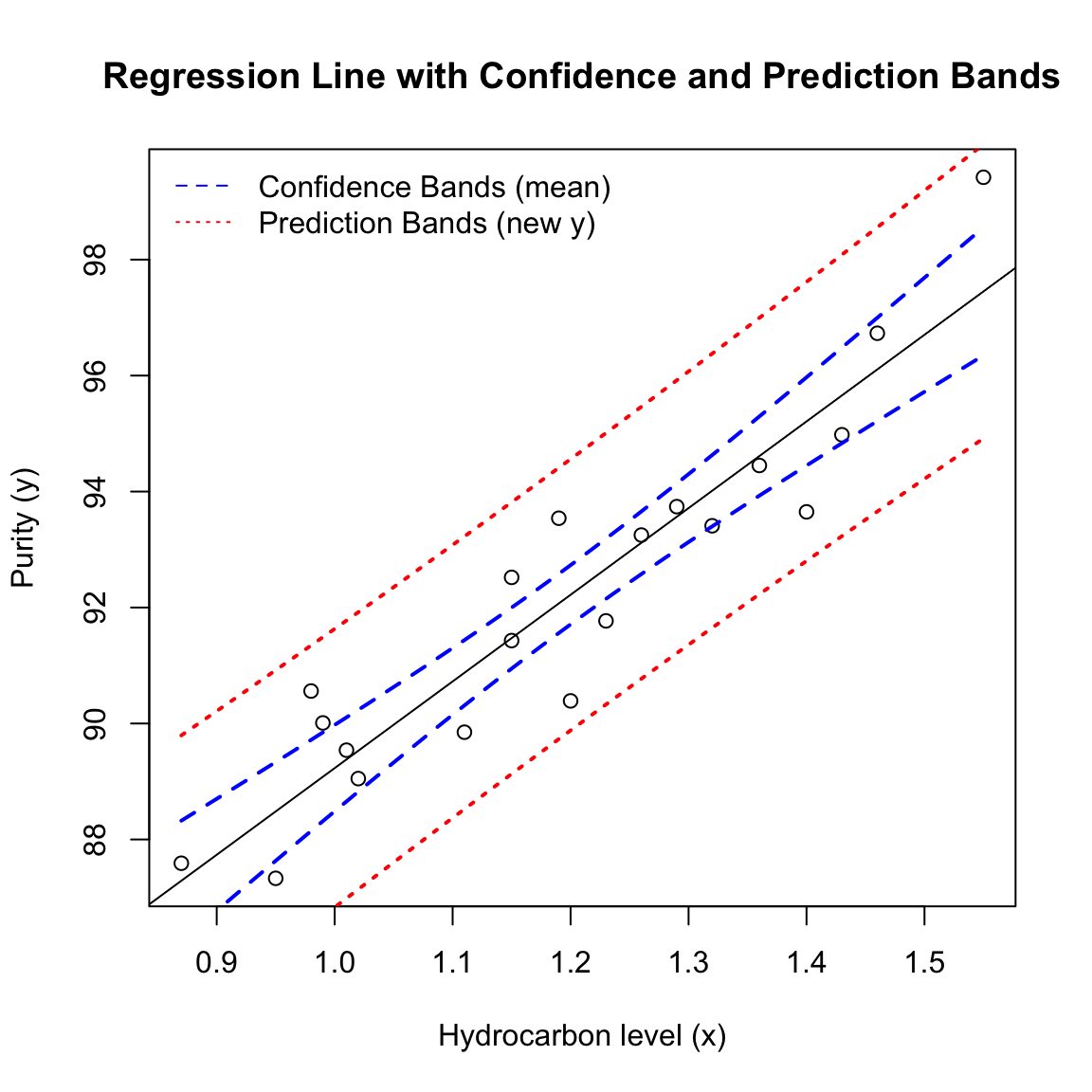

x 12.18107 17.71389anova(fit)The mean-response CI narrows near \(\bar x\) and widens at the extremes; the prediction band is wider by the irreducible noise term.

x0 <- seq(min(purity.data$x), max(purity.data$x), length = 50)

newdata <- data.frame(x = x0)

est.mean <- predict(fit, newdata = newdata, interval = "confidence", level = 0.95)

pred.new <- predict(fit, newdata = newdata, interval = "prediction", level = 0.95)plot(purity.data$x, purity.data$y,

xlab = "Hydrocarbon level (x)", ylab = "Purity (y)",

main = "Regression Line with Confidence and Prediction Bands")

abline(fit)

matlines(x0, est.mean[, 2:3], col = "blue", lty = 2, lwd = 2)

matlines(x0, pred.new[, 2:3], col = "red", lty = 3, lwd = 2)

legend("topleft", c("Confidence Bands (mean)", "Prediction Bands (new y)"),

col = c("blue", "red"), lty = 2:3, bty = "n")

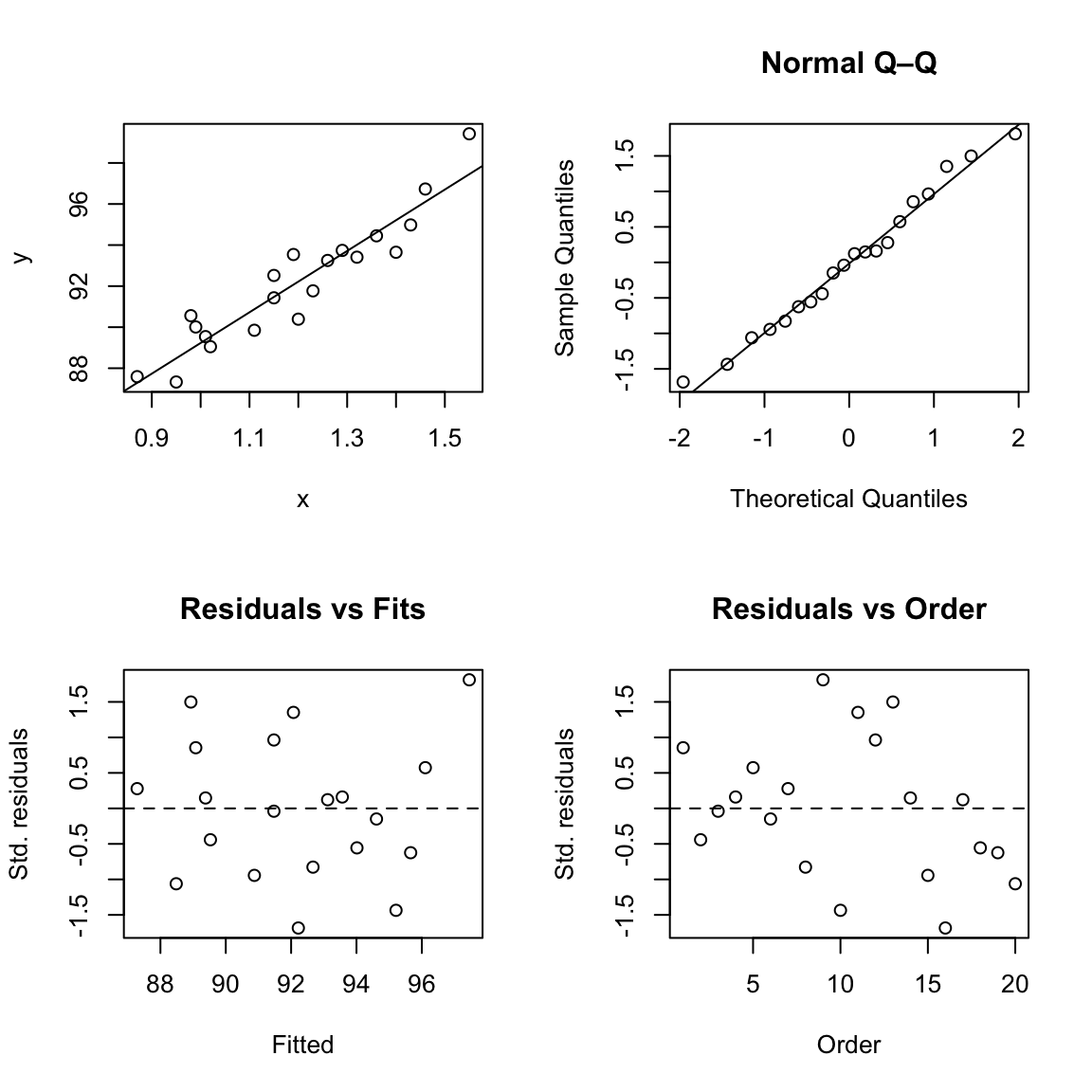

We look for no pattern in residuals vs. fits and approximate straightness in the Q–Q plot.

pred <- fitted.values(fit)

e <- resid(fit)

d <- e / summary(fit)$sigma

par(mfrow = c(2,2))

plot(purity.data$x, purity.data$y, xlab = "x", ylab = "y"); abline(fit)

qqnorm(d, main = "Normal Q–Q"); qqline(d)

plot(pred, d, xlab = "Fitted", ylab = "Std. residuals", main = "Residuals vs Fits"); abline(h = 0, lty = 2)

plot(1:n, d, xlab = "Order", ylab = "Std. residuals", main = "Residuals vs Order"); abline(h = 0, lty = 2)

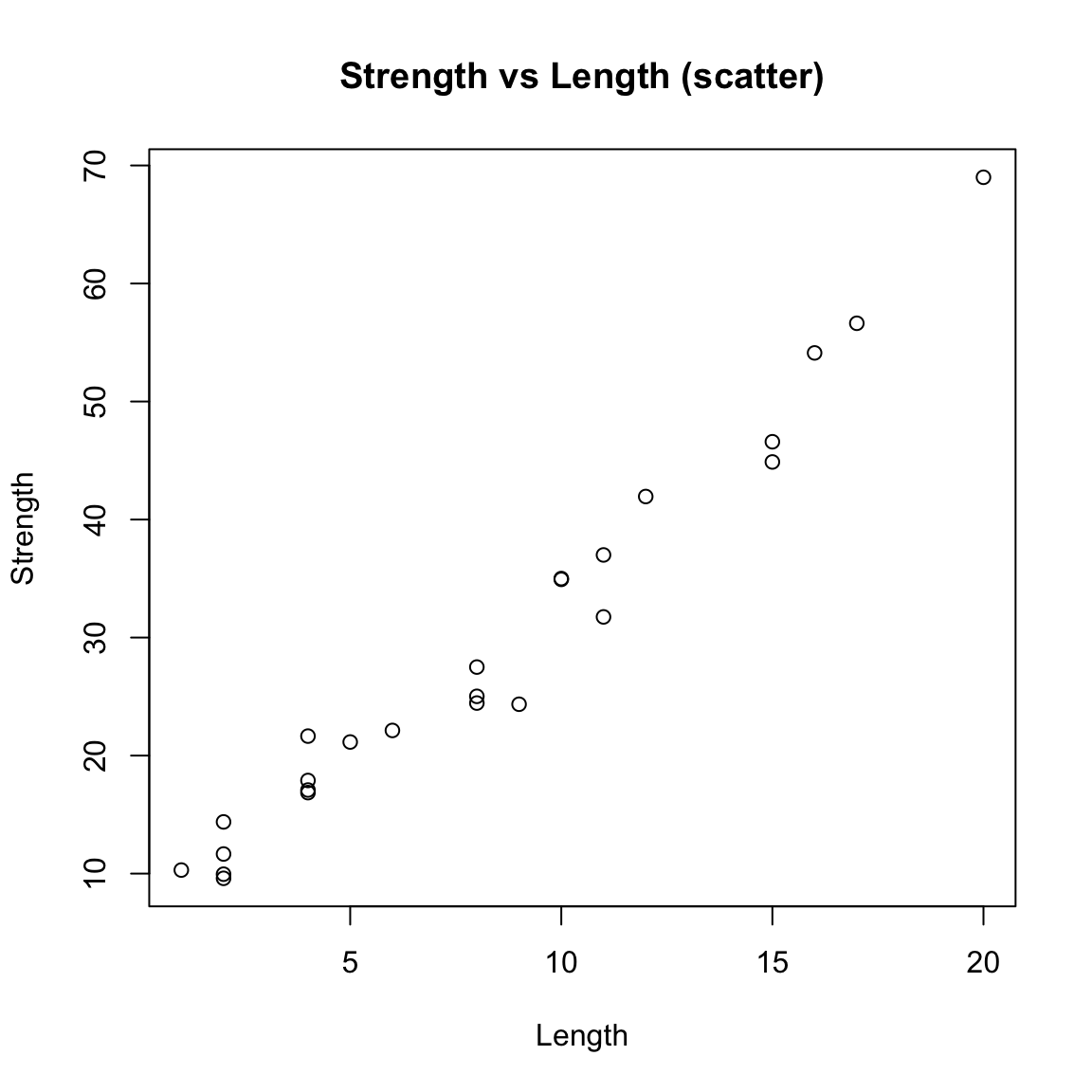

par(mfrow = c(1,1))Correlation summarizes linear association without fitting a line or making model assumptions.

strength <- c(9.95,24.45,31.75,35.00,25.02,16.86,14.38,9.60,24.35,

27.50,17.08,37.00,41.95,11.66,21.65,17.89,69.00,10.30,

34.93,46.59,44.88,54.12,56.63,22.13,21.15)

length <- c(2,8,11,10,8,4,2,2,9,8,4,11,12,2,4,4,20,1,10,

15,15,16,17,6,5)

plot(length, strength, xlab = "Length", ylab = "Strength",

main = "Strength vs Length (scatter)")

cor(strength, length)[1] 0.9818118cor.test(strength, length)

Pearson's product-moment correlation

data: strength and length

t = 24.801, df = 23, p-value < 2.2e-16

alternative hypothesis: true correlation is not equal to 0

95 percent confidence interval:

0.9585414 0.9920735

sample estimates:

cor

0.9818118 Note. A large \(|r|\) and small \(p\) indicate linear association; regression further quantifies the slope and supports prediction, with diagnostics to check assumptions.